How Your Driving Record Affects Car Insurance Premiums in the USA

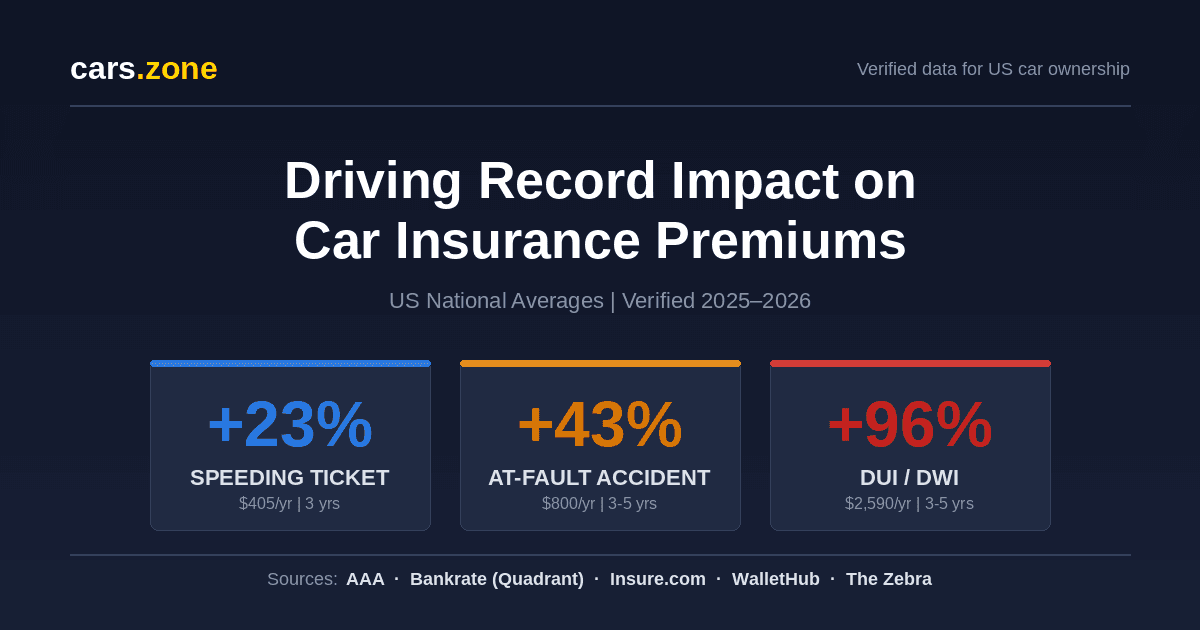

A single speeding ticket adds about $523/year to your full-coverage premium per Bankrate’s 2024 True Cost of Auto Insurance report — roughly $1569 over the typical 3 years it stays on your record. Experian’s January 2025 data puts the increase at 27.0%[Experian] (about $582/year). A DUI nearly doubles the average premium, taking it from $2697 to $5287[Bankrate]/year per Bankrate’s November 2025 analysis — a +96.0%[Bankrate] increase that sticks for 3 to 5 years (10 in CA, NV, MA). The pattern across all violations: insurance carriers have a long memory.

What a Single Driving Record Event Actually Costs Over 3 Years

Most drivers underestimate how long an insurance surcharge stays on file. The headline figure (the percent your premium goes up) is what carriers report. The number that matters is the multi-year cost.

The average US driver pays $2,697[Bankrate]/year for full-coverage car insurance per Bankrate’s November 2025 nationwide survey. Add a single moving violation and that average can jump 15–30% overnight, locked in for 3 to 5 years before falling off your motor vehicle record (MVR).

| Violation | Premium Increase % | Dollar / Year | 3-Year Cost | Stays on Record |

|---|---|---|---|---|

| DUI / DWI | +96.0% | ~$2590 | ~$7,770 | 3–5 yrs (10 in CA, NV, MA) |

| Reckless Driving | +91.0% | ~$1734 | ~$5,202 | 3 yrs |

| Hit-and-Run | +70.0% | ~$1077 | ~$3,231 | 3–5 yrs |

| At-Fault Accident | +43.0% | ~$1,165 | ~$3,495 | 3–5 yrs |

| Speeding Ticket | +27.0% | ~$523 | ~$1569 | 3 yrs |

| Insurance Lapse | +6–15% | varies | varies | 1–3 yrs |

Sources: Bankrate Nov 2025 (Quadrant Information Services); WalletHub Feb 2026; Insure.com Feb 2026; The Zebra traffic-ticket impact study; Insurance.com 2025.

Bankrate, Experian, U.S. News, and Insure.com all publish surcharge data but use different sample profiles — different states, vehicles, coverage levels, and insurer panels. The pattern across all datasets is identical: DUI hits hardest, reckless second, hit-and-run third. Exact percentages are comparison points, not guarantees. Your actual surcharge depends on your ZIP code, prior record, and which carrier you’re with.

Speeding Tickets: The Most Common Surcharge

Per Experian’s January 2025 marketplace data, car insurance premiums increase by an average of 27.0%[Experian] — roughly $582 per year — after a single speeding ticket. Bankrate’s 2024 True Cost report puts the national dollar impact at $523/year (about $1569 over three years).

The surcharge typically lasts three years from your first policy renewal after conviction. Some states and carriers extend this to five years. Repeat offenses stack — two speeding tickets in three years can push the surcharge to 50% or more.

Bottom line on speeding tickets: +27.0% on premium nationally, locked in for 3 years per ticket.

At-Fault Accidents: The Multi-Year Hit

An at-fault accident adds 43.0%[Bankrate] to your full-coverage premium for 3 to 5 years per Bankrate’s November 2025 data. U.S. News rate analysis finds a comparable jump: ($2524 → $3836, a +52.0%[U.S. News] jump).

The at-fault surcharge cannot be removed early once applied. Some carriers offer “accident forgiveness” programs that prevent the first at-fault accident from triggering a surcharge — but these need to be enrolled BEFORE the accident, not after.

DUI / DWI: The Heaviest Surcharge

A single DUI takes the average annual premium to $5287 after one DUI — a +96.0% increase over the clean-record baseline of $2697. U.S. News rate analysis confirms a similar magnitude (+92.0%[U.S. News]). Insure.com’s February 2026 study reports the actual range across insurers and states is wider: 43.0% to 322.0%[Insure.com], with the typical driver paying about $1163 more per year.

California, Nevada, and Massachusetts keep DUI convictions on your driving record for 10 years instead of the typical 3 to 5. That doubles or triples the total surcharge cost over the life of the conviction. If you’re in one of these states, the multi-year math is roughly $2590/year × 10 = $25,900 in additional premiums before your record clears.

Other Major Violations: Reckless Driving and Hit-and-Run

Beyond DUI and at-fault accidents, two other categories produce some of the heaviest surcharges in the industry.

Reckless driving adds +91.0%[WalletHub] on average per WalletHub Feb 2026 (about $1734/year per Insurance.com). State range is wide — Texas around 41.0%, Hawaii up to 242.0%.

Hit-and-run adds +70.0%[The Zebra] on average per The Zebra’s traffic-ticket impact study — about $1077 more per year. This is the single highest single-violation surcharge across all studies.

Driving without insurance (lapse) adds +6–15% on average, varies by state. The lapse itself is treated as a separate underwriting risk, not a moving violation.

What You Can Do About It

The pattern across all violations: the insurance industry uses a long memory. A clean record after the surcharge window restores you to baseline pricing — but the surcharge years cost real money that can’t be recovered.

- Standard “good driver” discount: 10% to 20% off baseline once you’ve held a clean record 3+ years.

- Telematics / usage-based programs (Snapshot, Drivewise, Drive Safe & Save): additional 5% to 30% based on observed driving habits — but with the trade-off of data collection.

- Defensive driving course completion: 5% to 10% off, available in most states. Especially valuable for drivers under 25 and over 55.

- Shop your renewal: insurers price violations differently. What triggers a 30% surcharge at one carrier may trigger 15% at another. Get quotes from at least three carriers 30 days before renewal.

If your record clears between violations (3 years for speeding, 3-5 for accidents and DUIs in most states), you become eligible for clean-record pricing again at the next renewal. Most insurers also offer a “good driver discount” of 10% to 20% off baseline once you’ve held a clean record for 3+ years. The drop is not automatic — shop quotes 30 days before renewal to capture it.

How a Surcharge Compares to Total Annual Ownership Cost

Insurance is one of the five major lines in the AAA Your Driving Costs framework — alongside fuel, maintenance, depreciation, and finance/registration. The 2025 AAA average puts insurance at $1,694[AAA]/year against a total annual ownership cost of $11,577[AAA] — roughly 15% of the total budget for an average sedan driven 15,000 miles a year.

A driving record event that adds 30% to insurance moves that share to about 19–20% of total ownership cost. For drivers in higher-risk segments — younger drivers, EV owners (whose insurance baseline runs higher; see our EV vs gas car ownership cost comparison), or those in expensive states — the impact is proportionally larger.

What’s on Your Insurance Record (And How to See It)

Two reports drive your insurance pricing, and both are accessible to you directly:

- The MVR (Motor Vehicle Report) comes from your state DMV and shows convictions, license actions, and moving violations — typically over the past 3 to 5 years. Cost: typically $5–15 directly from your state DMV.

- The CLUE report (Comprehensive Loss Underwriting Exchange), maintained by LexisNexis, shows insurance claims history over the past 5 to 7 years regardless of fault. You can request your CLUE report free once a year directly from LexisNexis.

Reviewing both before your next renewal is the single most useful 30 minutes you can spend on your insurance bill. Errors on these reports are common, and disputed errors that get removed often produce immediate rate decreases.

Sources & Methodology

- Bankrate 2024 True Cost of Auto Insurance report (Quadrant Information Services) — speeding ticket +$523/yr national average. bankrate.com

- Bankrate November 2025 rate analysis (Quadrant Information Services) — at-fault accident +43.0%, DUI $2697 → $5287 (+96.0%). bankrate.com/insurance/car

- Experian, January 2025 marketplace data — speeding ticket +27.0% / +$582 average. experian.com

- U.S. News & World Report rate analysis — at-fault accident +52.0% ($2524 → $3836), DUI +92.0%.

- Insure.com, February 2026 — DUI range across insurers/states 43.0%–322.0%, typical driver +$1163. insure.com

- WalletHub, February 2026 — reckless driving +91.0% national, range 41.0% (TX) to 242.0% (HI). wallethub.com

- The Zebra, traffic-ticket impact study — hit-and-run +70.0% / +$1077. thezebra.com

- LexisNexis Risk Solutions — CLUE (Comprehensive Loss Underwriting Exchange) report methodology and consumer access.

- AAA, Your Driving Costs 2025 — insurance at $1,694/year, total ownership at $11,577/year (15,000 miles, average sedan).

All figures cross-referenced against original publisher datasets. Last verified May 2026.

Frequently Asked Questions

About the Author — Ashvin J. Sonani

Founder & Lead Researcher at Cars.Zone. Digital marketer, data analyst, and domain investor with 28+ years of internet experience — from the pre-Google era of Lycos and Altavista through ecommerce operations (2000–2018) to current focus on US automotive cost intelligence. Specializes in extracting actionable conclusions from complex, multi-variable datasets across insurance, depreciation, and total cost of ownership. Cars.Zone analyses are built from primary industry sources (AAA, Kelley Blue Book, Edmunds, Experian, Bankrate) — never aggregator summaries — and cross-verified before publication. No manufacturer or dealer relationships influence editorial content.